Sunday, April 26th, 2026

Writing to you from Uruguay

It’s a big transition to go from an action packed cycle like the Fighter Cycle to another that really only requires study at a desk.

With all the wild things that have happened in the past couple months, the slow pace is welcome. Beyond that, I think that this is actually a great method: undergo a period of high volume action and then transition to a slower paced period of intense study on a new subject.

Fast-paced living creates a desire for the inverse and vice versa.

Anyway…

This first week in the Investor Cycle of The Preparation has actually been really good. It’s reminded me of when I was studying the fundamentals of economics a couple years ago. I’ve been learning new terms that help me better understand investing as a whole, but on top of that I think I’m starting to develop a new way of seeing the world—similar to how a new entrepreneur looks at the world through a new lens after making his first sale.

Of course, I have a long way to go and this is only the beginning in terms of “knowing how to invest”, but it’s enjoyable to get a handle on something I didn’t understand at all not too long ago.

What I’ve been learning about

Now, there’s a ton of terms I’ve learned from Stock Market Investing for Beginners course on Udemy—terms to describe different types of stocks, indices, methods of investing, or types of companies. It’s not worth taking the time to define a list of fairly simple terms. Instead, I’d rather stick to the interesting stuff.

I don’t want to bore you by explaining what the Dow Jones is or why you should buy a value stock instead of a growth stock.

While I did learn a lot of basic things that I didn’t previously understand from the Udemy course, the more valuable things I learned this past week came from talking to my dad about the book The Intelligent Investor by Benjamin Graham. Going over a couple chapters of the book with him allowed me to learn much more than I would have otherwise. He was able to explain things like bonds, quantitative easing, the bond price to yield ratio, and a number of other things like that.

Government Bonds

Bonds are oddly difficult to understand and I can’t say that I understand the entire concept yet, but let me try to explain the basics.

Essentially, government bonds are loans that people or institutions make to a government. When you buy one, you are giving the government money now, and in return the government promises to pay you interest and give back the original amount later. Governments use bonds to raise money for things like roads, wars, public programs, or paying existing debts. They are often considered relatively safe because they are backed by the government’s ability to tax, borrow, or print money.

It’s funny that they seem safe for those reasons because the government’s methods for maintaining the bonds involve taking money away from people (taxes), by devaluing the currency by printing more money, or by borrowing (creating debt and an obligation to print more money to pay that debt).

To my understanding, government bonds are debt created by the government. The investor, by putting his money into bonds, is choosing to pay for a portion of that debt now and is promised that he will collect a percentage in interest based upon the price he bought the bonds at. The idea is to help the government pay a debt while benefiting the investor, but it screws everybody in the long run.

After all, how could somebody create debt by using money to pay for debt or services using newly printed or borrowed money, pay back their investor using debt, and generate even more debt by printing or borrowing money to pay interest to their investor?

Perhaps there’s something I’m not understanding. To me, this is nothing short of entirely immoral. It’s a great way to make sure the dollar means less and less by the week.

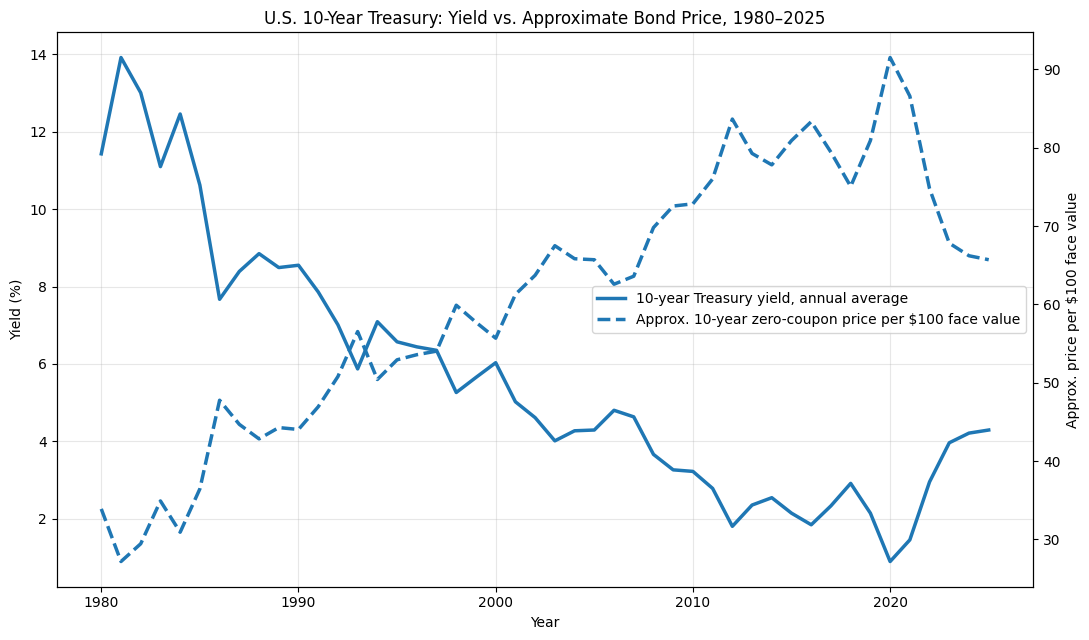

I’ll get back to this in a second, but let’s take a look at why you can make a lot of money if you invest in government bonds at the right time.

This graph is interesting because, although not totally accurate in terms of bond prices and yield rates, it shows you the bond price to yield ratio. When bond prices get higher, the yield rates go lower and vice versa. If you invested $10,000 in 10-year treasury bonds at their peak yield (15.32%) in September of 1981 you would walk away with your original 10k plus $15,320 in interest. That’s $1,532 in interest per year.

A 15.32% guaranteed return every year (as long as you don’t pull out of the investment before the end of the 10-year mark) is a fantastic investment.

(One quick point to make things clear: if you invested in 10-year treasury bonds at the 15.32% for yields in 1981, you’re investment would draw a return of 15.32% every year. No matter how much the market may fluctuate you will receive a fixed-rate return based upon the price you bought the bonds.)

Bonds, as I said, can be a great investment. However, they are one of the 3 main ways that our money is inflated away. Debt can’t be paid with debt that paid for debt that paid for debt…

So, just remember that this is one of 3 ways that the government destroys the value of the dollar. Why can you afford less and less every year? Why is everything so expensive? Why can’t your money take you very far?

This is one of the reasons.

Dividends

Dividends are much easier to understand than bonds.

Some companies will pay you back a percentage of their profits (dividends) for investing into the company. These are paid annually, semi-annually, or quarterly and can allow you to make money even when you invest in a company with a stable stock price.

Actually, dividends are a sign that a company has long-term thinking.

When a company pays dividends it’s a signal to investors that the business wants to create a symbiotic, mutually beneficial relationship. If you invest in our business you’re giving us an opportunity to be more successful in the future, so to incentivize you to continue your support we are going to pay you a percentage of our profits.

You benefit.

I benefit.

Everyone benefits.

On the other side of things, a lot of companies will buy shares of their own stock to drive up market prices, creating an illusion of greater success and a desire within people to get in before the stock prices get higher.

There’s a major problem with this: the people who invest in your business have no reason to watch your company succeed other than to watch the stock price reach a point where they’ll be satisfied to recoup their investment (plus profits). Through this method, people benefit when they sell their shares of your company—when they no longer have a stake in your success. Dividends promote the opposite.

Honorable mentions for other terms I learned:

ETF

Long vs. short

The 3 main forms of inflation

This came up during the conversations with my dad. I think this is important because it changes the way you look at the world, and investing itself. The knowledge of these forces, and how much they affect your life, changes how you look at making and managing money.

So, there are 3 forms of inflation: Bonds (which we already spoke about), fractional reserve banking, and quantitative easing.

Let me go over these quickly…

Fractional reserve banking: A quick summary doesn’t do it justice. You’d need to spend hours to understand it all and how screwed up it is. Fractional reserve banking is a system where banks keep only a fraction of customer deposits available as reserves and lend out the rest. For example, if you deposit $1,000, the bank may keep some on hand and lend most of it to someone else. That borrower then spends it, the money gets deposited again, and the process repeats. This expands the amount of “money” circulating in the economy through bank credit.

This can contribute to inflation because it increases the supply of money and credit faster than the supply of goods and services.

If the reserve requirement were 10%, then your $1,000 deposit could support up to about $900 of new lending by your bank. If that $900 gets deposited into another bank, that bank could lend $810, then the next could lend $729, and so on. But, the reserve requirement in the U.S. is 0%…meaning that banks aren’t required to hold onto any of your $1,000—they can lend a huge portion of it.

Here’s the catch: you can go back and withdraw you’re $1k at any time, but the money the bank created out of thin air as a “loan” to someone else is still in existence. So, new money was added to the money supply. Each dollar created means each dollar means less.

It’s a complex concept, but an example of how broken things are.

Quantitative easing: is when a central bank creates new money electronically and uses it to buy financial assets, usually government bonds (literally printing money to buy debt). It does this when it wants to push more money into the financial system, especially during a crisis or recession like the financial crisis of 2008.

Here’s the simple version: the central bank buys bonds from banks or investors. Those banks and investors now have more cash. That extra cash is supposed to make lending easier, lower interest rates, raise asset prices, and encourage people and businesses to borrow, invest, and spend.

QE “stimulates” the economy in the short term during a crisis. In reality, QE just makes an inevitable crisis worse.

A change in thinking

With these 3 main causes of inflation, the devaluation of the dollar, and the chaos in the world, it’s basically impossible to make any long-term investments.

Wars start and end (affecting economies) erratically. The financial system is its own terrible ponzi scheme. The devaluation of the dollar by inflation outpaces the financial benefits of much long-term investing.

Short-term, speculative trading is necessary to properly counteract the devaluation of your dollar.

2nd and 3rd order consequences

As I’ve learned, perhaps one of the most important—if not the most important—skill one needs for investing is the ability to see and understand the 2nd and 3rd order consequences from an economic event.

If you play chess you’ll get it…

My dad and I walked through the exercise of looking at how the closing of the Strait of Hormuz could impact the price of coal and, working on the assumption that coal will increase in price, which coal producers would be best to invest in. To be specific, we focused on the impact it could have in Asia and parts of Europe.

First, it was necessary to understand why coal could go up: a lot of liquid natural gas used to supply Asia and parts of Europe goes through the strait. Some of Qatar’s natural gas plants were damaged recently and will take 3-5 years to put back online. Qatar exports 20% of all the world’s LNG and 80% of all of that goes to Asia. 10-15% goes to parts of Europe. So, with that in mind, and the likelihood that the strait is closed for a prolonged period, there is an energy crisis on our hands. Coal would be, and already is, becoming necessary for many countries.

Japan is already trying to maximize its coal usage to reduce natural gas usage. Thailand is reopening decommissioned coal plants. Korea has lifted its 80% cap on coal-fired generation and suspended its efforts to reduce coal plants in the country.

That’s just a snapshot of what we were looking at. I won’t get into the coal companies we were looking into at the moment since they’ll be used in the next issue for Crisis Investing.

The exercise was very helpful. Understanding the ripple effects of an economic event, political event, war, or government policy is key.

Activities

Worked out 6 out of 7 days

My workouts consist of some weight lifting, some running, and some at-home Muay Thai (which really just means hitting the heavy bag). Ever since going to Thailand, I’ve realized how important cardio is.

Chess practice 6 out of 7 days

I’m getting better. Recently, I’ve decided to take the advice of a chess master I’ve been able to play a few games with: play 30 minute games. They give you time to really think about things (i.e. the 2nd and 3rd order consequences of every move).

Guitar practice 6 out of 7 days

Not much to say about this. Just practicing some of the same songs I did a few months ago.

Reading

Continued reading The Intelligent Investor by Benjamin Graham

Started reading The Dao of Capital by Spitznagel

Started reading Ask Monty by Monty Roberts

Finished reading Hondo by Louis L’Amour

Are these updates informative? Are they useful? Entertaining?

Leave a comment below if you’ve got any suggestions or questions for me.

And don’t forget to send this to someone who might benefit.

I’ll see you next week.

-Maxim Benjamin Smith

I am acting as a guinea pig for a program which is meant to prepare young men for the future. This program is designed to be a replacement for the only three routes advertised to young men today - go to college, the military, or a dead-end job.

All of these typical routes of life are designed to shape us into cogs for a wheel that doesn’t serve us. Wasted time, debt, lack of skills, and a soul crushing job define many who follow the traditional route.

This program, which we can call “The Preparation”, is meant to guide young men on a path where they properly utilize their time to gain skills, build relationships, and reach a state of being truly educated. The Preparation is meant to set young men up for success.

What appeals to me about The Preparation is the idea of the type of man I could be. The path to becoming a skilled, dangerous, and competent man is much more clear now. I’ve always been impressed by characters like The Count of Monte Cristo, men who accumulated knowledge and skills over a long period of time and eventually became incredibly capable men.

Young men today do not have a guiding light. We have few mentors and no one to emulate. We have been told that there are only a few paths to success in this world. For intelligent and ambitious people - college is sold to us as the one true path. And yet that path seems completely uncertain today.

We desperately need something real to grab onto. I think this is it.

I’m putting the ideas into action. Will it work? I can’t be sure, but I’m doing my best. I’m more than 60 weeks into the program at this point. So far, so good.

You can follow me along as I follow the program. Each week, I summarize all that I did.

My objective in sharing this is three fold:

Documenting my progress holds me accountable.

I hope these updates will show other young men that there is another path we can take.

For the parents who stumble upon this log, I want to prove to you that telling your children that the conventional path - college, debt, and a job is not the foolproof path you think it is.

Hi Maxim. My name is Jason Janczak. I live in Madison, Wisconsin, and I have been trying to push my way through the program. I am in the middle of a self-made cycle to be a mechanic. I have taken a complete 180 degree turn in my life from working in a warehouse driving a forklift to now working in an auto shop, working my way to getting my certification. I guess what I am saying is thank you for doing this blog. It has kept me focused on my path. It reminds me that even through the dirt and the grease, that this hard work will be worth it in the end and I have much more to look forward to, including all of the learning that has yet to come!

Max,.... I am so glad that you are focusing on the markets and how to interpret investments by the world's events. You are so blessed to have your father to work with you on this. No one ever thought the markets were easy (if they have half a brain), and it takes years to understand trades. Glad your health is back on track, and that you are studying all this.